Our present system for delivering publicly funded education is in need of dramatic reform. Educational choice programs provide that reform as they shift the power from state boards of education and school districts to parents. Educational choice programs are growing in popularity with programs in more than half the states and Washington, DC.

As the nation’s leading legal advocate for educational choice—with more than 25 years of experience defending these programs against legal challenges, including two victories before the U.S. Supreme Court and 10 state supreme court victories—IJ is well-positioned to weigh in on the constitutionality of proposed legislation. IJ’s team of educational choice experts are always available to answer questions or address concerns.

IJ’s Educational Choice Team

Model Educational Choice Legislation

Need Help?

For decades, IJ’s attorneys have helped bulletproof educational choice initiatives.

School Choice Assistance

U.S. Supreme Court Cases

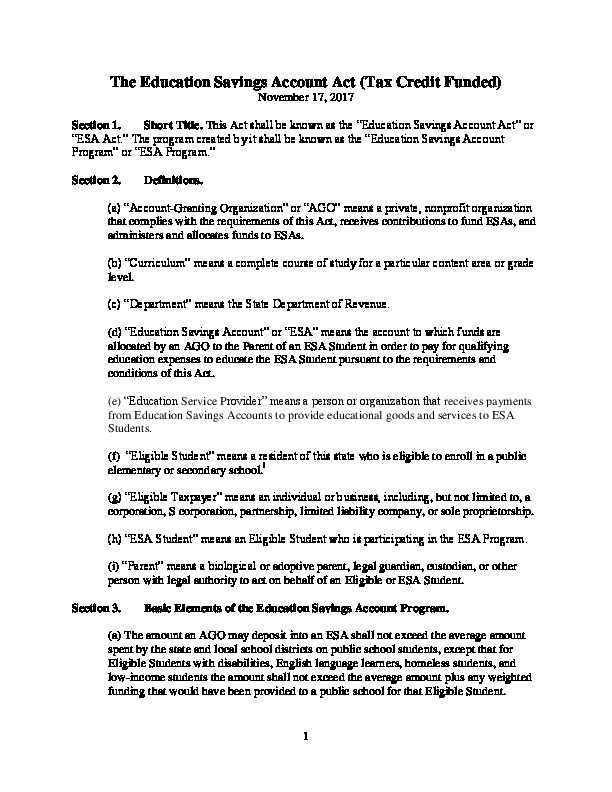

Educational Choice | Tax Credit Scholarships

Montana Moms Seek to Restore School Choice Program that was Struck Down for Including Religious Options

On June 30, 2020, the U.S. Supreme Court decided one of the most important education reform cases in the past half-century. This landmark case held that the U.S. Constitution does not allow states to discriminate…

Educational Choice Research

Educational Choice

A Guide to Designing Educational Choice Programs

Over the course of the last few decades, the law has gradually changed to recognize the constitutionality of educational choice programs and that its beneficiaries are students, not schools. The most recent development is Espinoza…

Educational Choice

Federal Special Education Law and State School Choice Programs

In this article, Nat Malkus and Tim Keller outline the federal laws that protect students with disabilities, give an overview of school choice programs, and explain how participating in school choice programs affects the rights…

Educational Choice

12 Myths and Realities about Private Educational Choice Programs

Educational choice programs—defined broadly as programs that provide parents financial aid to opt their children out of the traditional public school system—have been a topic of significant public discussion and debate in recent months. Despite…

Educational Choice

Bulletproofing School Choice

This paper brings together the hard-won lessons of IJ’s experiences to help advocates and lawmakers craft effective school choice legislation likely to withstand a legal challenge.