New Study Shows Arizona Tax Credits Serve Low- and Moderate-Income Families

Arlington, Va.—On November 3, the U.S. Supreme Court will hear the next big school choice case. A new study released today, which examines the Arizona choice program at the center of the legal fight, finds that the primary beneficiaries of the choice program are overwhelmingly students from low- and moderate-income families—a statistical fact that counters anecdotal findings by local newspapers.

The new study, which examines Arizona’s Individual Scholarship Tax Credit program—a program that will be the subject of a U.S. Supreme Court argument on Nov. 3, 2010—concludes that a majority of children receiving scholarships under the program are from low- and moderate-income families. The scholarship program permits taxpayers to claim a tax credit up to $500 for contributions to charities called School Tuition Organizations that use the funds to award private school scholarships. The study, authored by Vicki E. Murray, Ph.D., Education Studies Associate Director and a Senior Policy Fellow at the Pacific Research Institute, refutes allegations by the East Valley Tribune and the Arizona Republic that the program disproportionately serves students from wealthy families.

“Arizona’s Scholarship Tax Credit program is predominantly serving low- and middle-income families,” declared Dr. Murray. “There is no factual basis for claims that the scholarship program limits access to students from wealthy families.”

Dr. Murray’s working paper, An Analysis of Arizona Individual Income Tax-credit Scholarship Recipients’ Family Income, 2009-10 School Year, is available from Harvard University’s Program on Education Policy and Governance (PEPG) here: http://www.hks.harvard.edu/pepg/PDF/Papers/PEPG10-18_Murray.pdf. Dr. Murray collected family income and related data directly from School Tuition Organizations for 19,990 students, which represents nearly 80 percent of all scholarships awarded in 2009. By contrast, the East Valley Tribune and the Arizona Republic based their claims on interviews or related statistics from approximately 15 of the 55 School Tuition Organizations operating at the time. The newspapers did not collect student-level income data to verify their allegations. The student-level data Dr. Murray collected show:

- Scholarship recipients’ median family income was $55,458—nearly $5,000 lower than Arizona’s median income of $60,426, according to the U.S. Census Bureau. It was also nearly $5,000 lower than median incomes in recipients’ own neighborhoods, as estimated using student addresses and zip codes.

- The annual family income of more than two-thirds (66.8 percent) of scholarship recipients would qualify them for another of Arizona’s educational aid programs, the means-tested corporate tax credit scholarship program, eligibility for which is capped at $75,467 for a family of four.

- A higher proportion of scholarship recipients come from families whose incomes qualify them as poor (at or below $20,050 for a family of four) than the U.S. Census Bureau statewide average, 12.8 percent compared to 10.2 percent.

The study is released at a pivotal moment in the scholarship program’s 10-year history. The U.S. Supreme Court is scheduled to hear oral argument in Garriott v. Winn on Wednesday, November 3 at 10 a.m. Garriott is a legal challenge filed by the ACLU of Arizona claiming that the program is unconstitutional because a majority of taxpayers and parents have thus far chosen to contribute to religiously affiliated School Tuition Organizations and to enroll their children in religious private schools. The Institute for Justice is defending the program.

“The U.S. Supreme Court has repeatedly ruled that school choice programs based on private choice—where individuals rather than the government decide where scholarships are used—are perfectly constitutional,” declared Tim Keller, executive director of the Institute for Justice Arizona Chapter. “And private choice is the defining characteristic of Arizona’s tax credit program. Private individuals choose to set up scholarship organizations. Private individuals freely decide which organizations they donate to. And parents make the choice where to enroll their children. Private individuals are making these choices and the government remains completely neutral as to which School Tuition Organization a donor selects and which school a parent chooses.”

On Friday, IJ filed a reply brief in the Supreme Court relying on Dr. Murray’s study to refute some of the ACLU’s claims. IJ’s reply brief is available here: http://www.ij.org/images/pdf_folder/school_choice/arizona/ussc-winn-reply-ij.pdf. Other briefs filed in the case are available here: http://www.ij.org/Winn.

“Under the Constitution and well-established U.S. Supreme Court precedent, states are free to create programs that emphasize parental choice over centralized control and that include, among various educational options, private religious schools,” Keller concluded.

“Arizona’s Scholarship Program is not just a program of private choice,” Dr. Murray said. “It is a vital educational aid program that helps tens of thousands of low- and middle-income families pursue opportunities that would otherwise be foreclosed to them.”

Related Content

Related Reports

Educational Choice | Tax Credit Scholarships

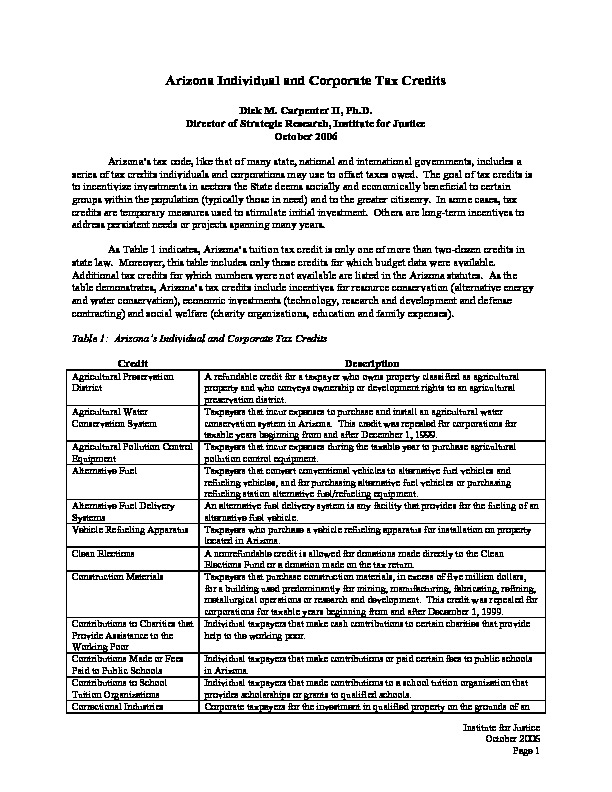

Arizona Individual and Corporate Tax Credits

Arizona’s tax code, like that of many state, national and international governments, includes a series of tax credits individuals and corporations may use to offset taxes owed. Arizona’s individual and corporate scholarship tax credit programs…