Eighty-eight-year-old retiree Tuncay Saydam is at risk of losing his life’s savings. Not because of a bad investment or a fraudulent scheme. Rather, the federal government is trying to fine Tuncay over $437,000—because he unintentionally failed to file a one-page form.

Born and raised in Turkey, Tuncay (pronounced Toon-jai) became an early academic pioneer of computer science. He, his wife, and his two daughters immigrated to the United States in 1980, where he worked as a professor at the University of Delaware for 25 years. He became a U.S. citizen along the way, though he retains his Turkish citizenship too, and he and his wife make monthslong trips back to Turkey each summer. He’s not rich, but because of his expertise, he was able to build up savings to comfortably fund his retirement. In other words, Tuncay thought he was living the American Dream.

While working overseas during sabbaticals, Tuncay also consulted for several Swiss communications companies. Tuncay stored those earnings at a bank in Switzerland, eventually growing it to about $500,000. And when the Swiss bank stopped doing business with U.S. residents, he moved it to a Turkish bank, and then to a bank back in America. To Tuncay, it was a nest egg—his life savings.

But Tuncay did not know he was violating federal law. Not by having a foreign bank account—there’s nothing illegal about that. But federal law requires people who own foreign bank accounts totaling more than $10,000 to file a short, annual report with the IRS, called the “FBAR.” It’s separate and apart from your obligation to pay income tax; it applies whether or not the foreign account makes any taxable income at all. And the maximum penalties can be exorbitant: either $100,000 or half the balance in the unreported account for each unfiled year, whichever is greater.

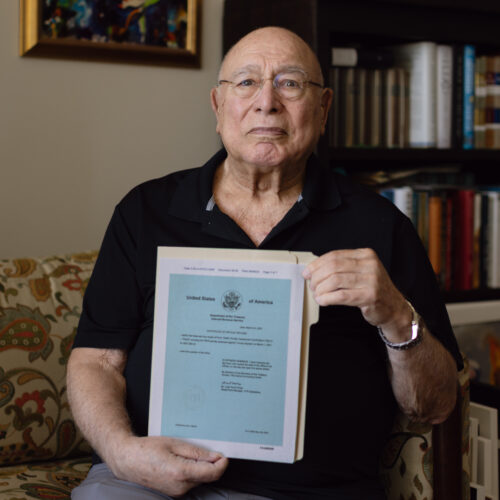

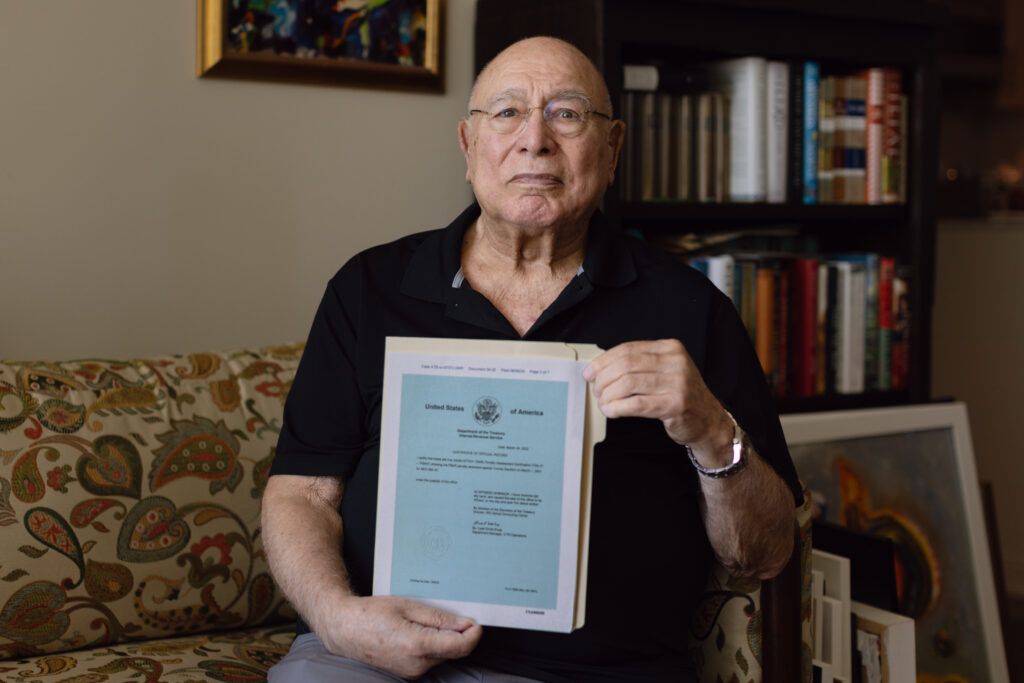

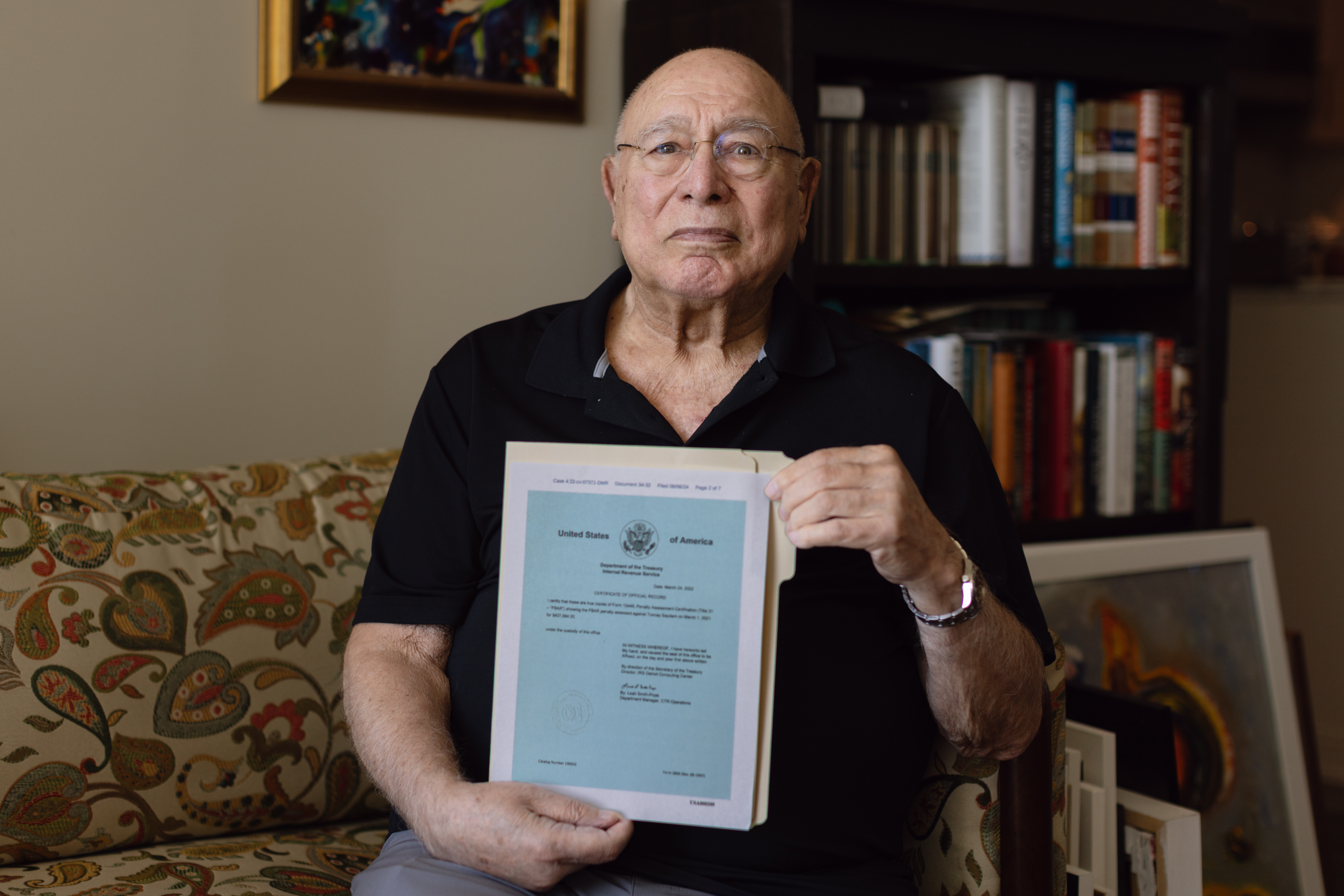

Tuncay fell victim to them. Tuncay owed the government around $29,000 in back taxes. To that, the IRS tacked on an additional $12,000 in penalties. But for the FBARs, the agency hit Tuncay with a separate, staggering fine: $437,564.

When the government sued Tuncay to collect on the $437,564.00, the district court rejected Tuncay’s defense under the Eighth Amendment’s Excessive Fines Clause. But Tuncay’s not giving up. Now, he’s teamed up with the Institute for Justice to appeal his case. The Excessive Fines Clause embodies a simple principle—the fine must fit the crime. And with a win, Tuncay could not only rein in the IRS’s use of runaway penalties for minor offenses (Tuncay is far from the only one the agency has targeted with this trap for the unwary), but also reinvigorate a critical constitutional safeguard for countless ordinary Americans.

Case Team

Clients

Case Documents

9th Circuit Opening Brief

Association of Americans Residents Overseas Amicus

Professor Beth Colgan Amicus

9th Circuit Reply Brief

Media Resources

Get in touch with the media contact and take a look at the image resources for the case.

Andrew Wimer Director of Media Relations [email protected]

Related News

Tuncay Saydam lives the American Dream

Tuncay embodies the American Dream. He was born aboard a ship in 1938 and raised, desperately poor, in the Turkish port city of Izmir. His father died when he was ten. Through hard work and perseverance—he did his schoolwork under a streetlamp because his childhood home lacked electricity—he eventually earned graduate degrees and became an early academic pioneer of computer science. For many years, he taught in Istanbul, becoming dean of engineering at Bosphorus University.

Then America was fortunate to have his talents. In the late 1970s, the University of Delaware recruited him as a tenured professor. So Tuncay, his wife Oya, and their two daughters moved to the United States. Tuncay and Oya were proud to become American citizens in the late 1980s. The judge presiding over the naturalization ceremony picked Tuncay to stand before the hundred-or-so new citizens to express how it felt to become an American.

Work-wise, he published six books and dozens of articles and gave lectures around the world. Family-wise, his two daughters started their own careers and families. Tuncay retired in 2005. Today, he and Oya live in a small condo in San Francisco, where Tuncay paints and goes to the opera, and he and Oya spend time with and are looked after by one of their daughters and her family.

The government’s “FBAR penalty” fines Tuncay out of most of his life’s savings

In the 1980s and ’90s, Tuncay took two sabbaticals to teach at universities in Switzerland, ETH Zurich and the École Polytechnique Fédérale de Lausanne. Also around that time, he worked as an engineering consultant with several Swiss telecommunications companies. The money he earned in Switzerland was deposited in a bank there, with Tuncay setting it aside as a future nest egg. Eventually, in 2012, the Swiss bank notified Tuncay that it was halting its business with Americans due to “tightening” U.S. “regulations.” Tuncay was in Turkey at the time (he remains a dual citizen), so he traveled to Zurich to close his account and transfer the $525,000 it contained to a bank in Turkey.

It is legal for Americans to hold funds in foreign bank accounts. Under the 1970 Bank Secrecy Act, however, Americans with foreign bank accounts containing over $10,000 must file annually a one-page “FBAR” form with the government. The main purpose of the FBAR is to catch transnational criminals. The form identifies basic information about the account, the filer, the bank, and the account’s maximum value during the reporting period. The requirement applies regardless of any taxable income the account accrues, if any. And if the government decides that a reporting violation was “willful”—a term that covers not just intentional violations, but objectively “reckless” ones too—the maximum penalties skyrocket: either $100,000 per report or half of whatever the unreported bank account contained for each unreported year. As the IRS’s National Taxpayer Advocate has written, the FBAR penalties are “among the harshest civil penalties the government may impose.”

Tuncay learned this the hard way. Until 2018, he had never heard of the FBAR requirement. That’s when the IRS began auditing him for FBAR compliance. At the end of the audit a full three years later, the IRS concluded that Tuncay had violated the FBAR requirement from 2013 to 2017 (prior years fell outside the statute of limitations), that he was reckless in not learning of the FBAR requirement, and that the agency was fining him an eye-watering sum as a penalty: $437,564. It imposed that sum even though Tuncay’s underpayment of taxes during that same period was a fraction of that total: just $29,006. And even though the government would separately impose a nearly $12,900 penalty for that tax deficiency itself.

The district court rejects Tuncay’s “excessive fines” claim, and he teams with IJ to seek the Ninth Circuit’s review

After imposing its nearly half-a-million dollar penalty, the government sued Tuncay in federal court to collect. As a defense, Tuncay invoked the Eighth Amendment’s Excessive Fines Clause. His argument was on strong footing. The Excessive Fines Clause, like its precursors in the English Bill of Rights and Magna Carta, enshrines a timeless teaching: The fine must fit the crime. And a runaway civil penalty for a minor reporting offense—which in no way compensates the government for financial loss—is just the sort of punishment the Excessive Fines Clause exists to check.

Even so, the district court rejected Tuncay’s excessiveness defense. In the court’s view, it owed special “deference” to the IRS’s assessment of an appropriate penalty. So long as the fine the agency imposed on Tuncay was not beyond the maximum penalty that Congress had allowed for FBAR violations, the court said, it was “not the court’s role” to “second-guess” that “wisdom.”

Tuncay has teamed up with IJ to challenge that ruling on appeal to the Ninth Circuit. The amount that the government is seeking to extract from Tuncay is wildly out of proportion with the gravity of his wrongdoing. And in the context of monetary punishments, deference to the executive branch’s judgments is exactly the opposite of what the Excessive Fines Clause demands. As Justice Scalia observed in the early 1990s, fines, unlike incarceration, are a “source of revenue” for the government. So, he warned, “[t]here is good reason to be concerned that fines, uniquely of all punishments, will be imposed in a measure out of accord with the penal goals of retribution and deterrence.” Those concerns have only multiplied in the decades since; nationwide, police, prosecutors, and bureaucrats alike rely on fines and forfeitures for their budgets. Indeed, from 2012 to 2020 alone, the IRS assessed nearly $1.5 billion in penalties for violations of the little-known FBAR requirement.

Making matters worse, the federal government often demands courts defer on whether FBAR penalties violate the Excessive Fines Clause while simultaneously insisting that the Excessive Fines Clause doesn’t apply to FBAR penalties in the first place. (They’re “penalties,” you see, not “fines.”) To its credit, the district court rejected that reasoning in Tuncay’s case. But across the nation, the government continues to press that view in FBAR cases. The Constitution’s Framers foresaw precisely this desire to unilaterally impose sky-high fines for small misdeeds. That’s why the Excessive Fines Clause is in the Bill of Rights, and that’s why courts in the 21st century—including in Tuncay’s case—must take the Excessive Fines Clause seriously.

About the Institute for Justice

The Institute for Justice (IJ) is a public-interest law firm that litigates nationwide to vindicate individual liberties. In 2019, IJ secured a Supreme Court victory holding that the Excessive Fines Clause applies to state and local governments, and in a 2023 IJ case, Justice Gorsuch voiced his dissent from the Court’s refusal to review the $2.17 million FBAR penalty imposed on another octogenarian. IJ is now seeking to protect an Alaska bush pilot’s $95,000 airplane from being forfeited because a passenger’s luggage contained some beer. IJ is also currently litigating to protect Detroiters targeted by Wayne County, Michigan’s forfeiture apparatus and thousands of Alabamians victimized by a notorious profit-fueled ticketing scheme in Brookside, Alabama.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}